Before you buy a car, make sure it is not tied to a car finance agreement that has not been settled. If you purchase a car that still belongs to a lender, the seller may not have had the lawful right to sell it in the first place. That means you could lose both the vehicle and the money you paid.

That is why an outstanding car finance check matters. At My Car Reg Check, we help you check if a car is on finance before you commit to a sale, so you are not left dealing with someone else’s financial responsibility after the handover. A simple vehicle finance check can show whether the car is linked to active finance and whether there is a risk attached to the purchase.

This is especially important when you are dealing with a private seller. A car with outstanding finance can look completely normal and drive well, yet still cause a serious ownership problem after you have paid for it. Many buyers only discover the problem after they have already paid for the car and completed the purchase.

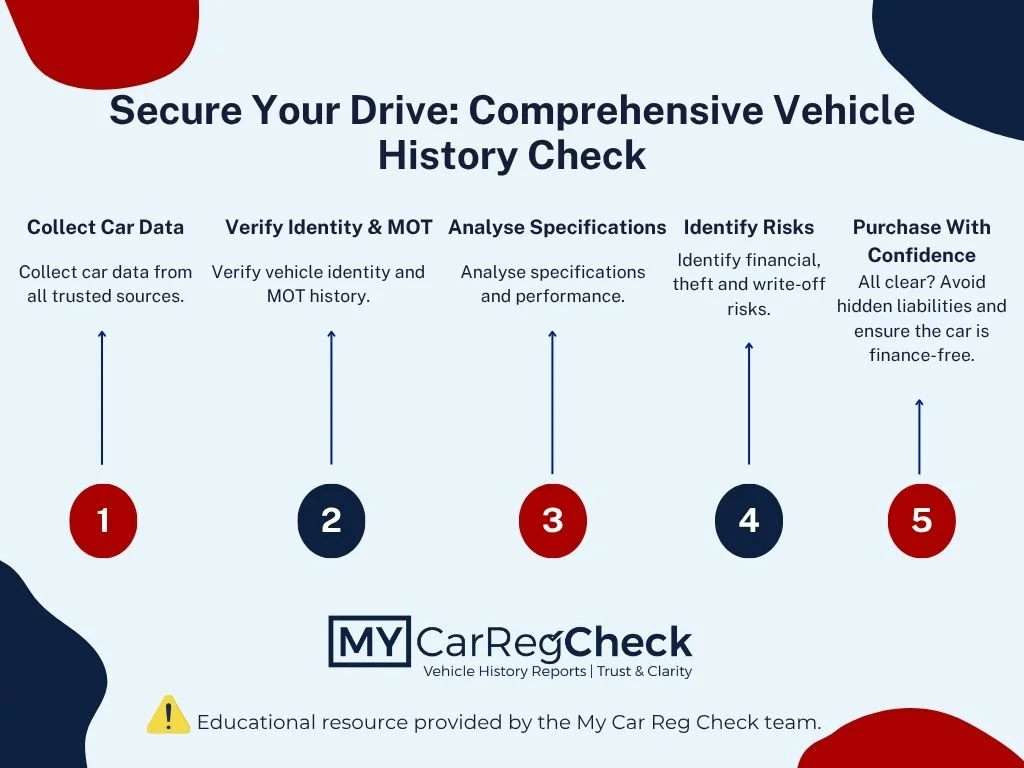

How To Avoid Buying a Car With Outstanding Finance (infographic)

⚠️ Important: Being the 'Keeper' isn't the same as being the 'Owner.'

It is a common misconception that the V5C logbook acts as a title deed. In reality, the V5C simply registers the person responsible for the car’s tax and official paperwork. If there is an active finance agreement in place, the finance company is the true legal owner, even if the seller’s name is on the logbook. To build a full picture before buying, it can also help to review the previous keeper history.

Our finance checker is designed to help you spot that risk early. If you want to check outstanding finance on car records before you hand over any money, starting with a free car check is a sensible first step. If you need more reassurance before you buy a vehicle, checking its vehicle history can help you review the car with more confidence.

What is an Outstanding Finance check?

An outstanding finance check tells you whether there is still a loan linked to a vehicle. When you use our Car Finance Checker, we check relevant finance records against the vehicle details after entering the registration, so you can see whether a lender still has a legal claim over the car.

A proper finance check on a car search does more than give you a yes-or-no result. It can also show useful details such as the agreement date, agreement type, agreement term, the finance company, and relevant contact details linked to the agreement.

This matters because paperwork can be misleading if you do not know what it proves. The V5C logbook shows who is responsible for registering and taxing the vehicle, but it does not confirm legal ownership. A DVLA record can help you verify registered keeper details, but it still does not prove the seller owns the car outright.

That is why buyers should not rely on the logbook alone. Even if the seller has the V5C in hand, a finance check on vehicle records can still show if there is an active finance agreement on the car. Checks such as V5C serial number verification are useful for document checks, but they are not a substitute for checking whether finance is still attached to the vehicle.

The Financial Risk: What Happens if You Buy a Financed Car?

The biggest financial risk is simple: you pay for the car, but the seller may not have had the legal right to sell it. With common finance products such as Hire Purchase and PCP, the lender usually keeps legal title to the vehicle until the agreement is settled in full. That means the car is still treated as the finance company’s asset, even if it is being driven by the person selling it to you.

If the seller falls behind with payments or stops paying altogether, the lender can take action to recover its asset. In practice, this means the lender could repossess the car from you, even if you bought it in good faith. This is why an unpaid finance agreement is not a minor paperwork issue. It is a legal ownership problem.

A common mistake buyers make is focusing only on the condition of the car and the price. Imagine you buy a used car privately, drive it home, insure it, and think the deal is done. A few weeks later, the lender contacts you because the seller has defaulted on the finance agreement. You are now caught in a dispute over an asset the seller did not own outright.

This is also why checking the logbook is not enough on its own. The V5C does not override the lender’s legal interest under HP or PCP. Before you agree to buy, it is worth using a free car finance check and a stolen car check to reduce the chance of walking into that kind of loss.

What Types of Finance Will This Report Reveal?

An outstanding finance report is not restricted to a single type of borrowing. At My Car Reg Check, we look for the most common types of secured vehicle financing that can impact legal ownership, resale rights, and buyer risk. That matters because different agreements work in different ways, but the result for a buyer can be the same: the seller may not own the car outright.

The most common finance types a report can reveal include:

- Hire Purchase (HP): With HP, the finance company typically retains legal title to the vehicle until the final payment is made. The person driving the car is contributing to ownership, but they are not yet the legal owner.

- Personal Contract Purchase (PCP): PCP is one of the most common ways cars are funded in the UK. Monthly payments are often lower, but legal ownership normally stays with the lender unless the agreement is completed and any final balloon payment is dealt with.

- Lease Purchase (LP): This works in a similar way to other secured finance arrangements, where the borrower pays in stages and ownership does not pass over until the agreement terms are fully met. From a buyer’s point of view, the key issue is the same: the vehicle may still be tied to finance.

- Logbook Loans (Bill of Sale): These are especially important to spot because they can be easy for buyers to miss. Because the loan is secured against the car, a buyer could end up purchasing a vehicle that the seller does not fully have the right to sell.

- Unit Stocking (Dealership Finance): This is finance used by dealerships to fund the cars they keep in stock. It is less commonly discussed by buyers, but it still matters because it can affect whether a vehicle is clear to be sold properly.

This is why a proper finance report adds real value beyond a visual inspection or a look at the logbook. Two cars can look identical on the driveway, but one may still be subject to financing that creates a legal and financial problem after purchase. If you want to start with a simple first step, our free car finance checker can help you screen a vehicle before deciding whether you also need an insurance write-off check.

What Finance Agreements Are NOT Included?

Not every loan used to buy a car is registered against the vehicle. The main example is an unsecured personal bank loan, where the seller borrowed money in their own name and then used that money to buy the car.

In that situation, the loan normally belongs to the person, not the vehicle. The car is not usually secured for the loan, so it should not appear as an outstanding finance marker on a car finance check.

This is different from HP, PCP, lease purchase, or a logbook loan. With those agreements, the finance company may still have a legal interest in the car until the agreement is settled and paid off in full.

A simple example is this: a seller takes a £10,000 personal loan from their bank, buys a used car outright, and later sells the car privately. They may still owe money to the bank, and that loan may affect their credit report or credit score, but the car itself is not normally tied to that loan.

In these cases, the seller usually has legal title to the vehicle. That means the car legally belongs to them, and they can normally sell it without needing permission from the lender.

This is why an outstanding finance check should be understood properly. If our car finance checker does not show an active finance agreement, that does not mean the seller has no personal loans at all. It means no secured finance agreement has been found against the vehicle records we checked.

As a buyer, your focus should be on whether the vehicle itself is tied to a lender. A private personal loan may still be the seller’s responsibility, but it does not usually give the bank the right to repossess the car from you after purchase.

That said, you should still look at the whole picture before buying. If the seller’s story keeps changing, the V5C details do not match, or the price seems unusually low, treat it as a warning sign and carry out a wider UK car history check before paying.

If you are unsure, ask the seller a clear question: “Was this car bought using HP, PCP, lease purchase, logbook loan, or only a personal bank loan?” An honest seller should be able to explain the difference and provide supporting documents where needed.

For extra peace of mind, keep written proof of the seller’s explanation, payment receipt, advert, and any messages. If something does not add up later, you can also check independent consumer guidance from

Citizens Advice

before deciding what to do next.

Data Accuracy: “Finance Cleared” vs. “Finance Fully Closed”

A finance record does not always update the moment a payment is made. It depends on when the lender or finance company updates its system, so a car may still show as financed for a short time after the seller has paid it off.

For example, a seller may have settled the outstanding balance yesterday, but the vehicle could still appear as “outstanding” today. That does not always mean the seller is lying, but it does mean you should not rely on their word alone.

There is an important difference between finance being paid and finance being formally closed. A payment may have been made, but the lender still needs to apply the funds, update the agreement, and close the account properly.

If you use My Car Reg Check to check your target car for outstanding finance, and the result still shows finance after the seller says it has been cleared, pause the purchase. Ask the seller to provide proof from the lender before you hand over any money.

A genuine seller should understand this. If they have paid the finance, they should be able to contact the lender and get written confirmation that the account is fully closed or in the process of being updated.

Until the finance company has formally closed the agreement, there may still be uncertainty around the vehicle’s status. That uncertainty matters because the lender may still appear to have an interest in the car until the records are updated.

If there is a disagreement about whether the finance has been settled, ask for direct confirmation from the finance company, where possible. If the issue becomes a formal complaint about how the lender has managed or reported the agreement, the Financial Ombudsman Service may be able to help. However, before buying, your first priority should be to get clear written proof of the car’s finance status.

What to Do If Your Check Shows Active Finance

If your check shows active finance, pause the sale straight away. Do not hand over cash, send a bank transfer, sign a receipt, or agree to “sort it later” once the car is in your name.

Active finance does not always mean the seller is trying to mislead you, but it does mean the vehicle may still be linked to a finance company. Before you continue, the position must be clear in writing.

Follow these steps before making any decision:

- Ask the seller to contact their lender and request a formal settlement figure.

- Check that the settlement figure is recent and comes directly from the finance company.

- Do not pay the outstanding balance to the seller and trust them to clear it later.

- If you proceed, arrange for the finance balance to be paid directly to the finance company.

- Only pay the seller any remaining amount after the finance has been settled.

- Ask for written confirmation that the agreement has been paid off and closed.

- Run another check before collection to confirm the vehicle no longer shows active finance.

- Keep copies of the advert, receipt, seller messages, finance letters, and payment proof.

It is also worth checking whether the agreed sale price makes sense. If the seller is asking for much less than the car is worth, get a professional valuation before you continue, as a very low price can sometimes be a warning sign.

If the seller refuses to cooperate, pressures you to pay quickly, or says the finance is “nothing to worry about,” walk away. A genuine seller should understand why you need the finance cleared properly before buying.

Frequently Asked Questions

Is it illegal for a seller to sell a car on finance?

A seller should not sell a car on active finance as if they own it outright. With finance such as HP or PCP, the finance company may still be the legal owner until the agreement is settled.

If the seller hides the finance, gives false information, or takes your money knowing they had no lawful right to sell, that can become a serious legal issue. The safest step is simple: do not buy until the finance company confirms the agreement has been cleared.

Does the Hire Purchase Act 1964 protect me?

The Hire Purchase Act 1964 can protect some private buyers who bought a car in good faith without knowing it was still on hire purchase or conditional sale. This is often described as the buyer gaining “good title” to the car.

However, this protection is not automatic in every situation. If your check already shows active finance before you buy, you now know there is a problem, so you should not rely on this protection as a backup plan.

Can I find out the exact settlement figure?

Usually, no. The exact settlement figure normally has to come from the seller, because they are the agreement holder, and the finance company may not share private account details with you.

The settlement amount can depend on the outstanding balance, fees, payment date, and sometimes the interest rate or early settlement terms. Ask the seller to request a written settlement figure from the lender, and if you proceed, pay the finance company directly rather than trusting the seller to clear it later.